From Cards to Control: How Capital One and Brex Will Influence Merchant Cash Flow

- Trevor Johnson

- Jan 26

- 6 min read

Capital One’s move to acquire Brex for $5.15 billion is a bid to control the operating system of U.S. business spending, not just to add another card portfolio. Announced alongside Capital One’s latest earnings and slated to close later this year subject to approvals, the deal builds on the Discover acquisition and pushes the bank toward a single, technology‑driven stack that runs from network to software and sits in the middle of how businesses pay and get paid.

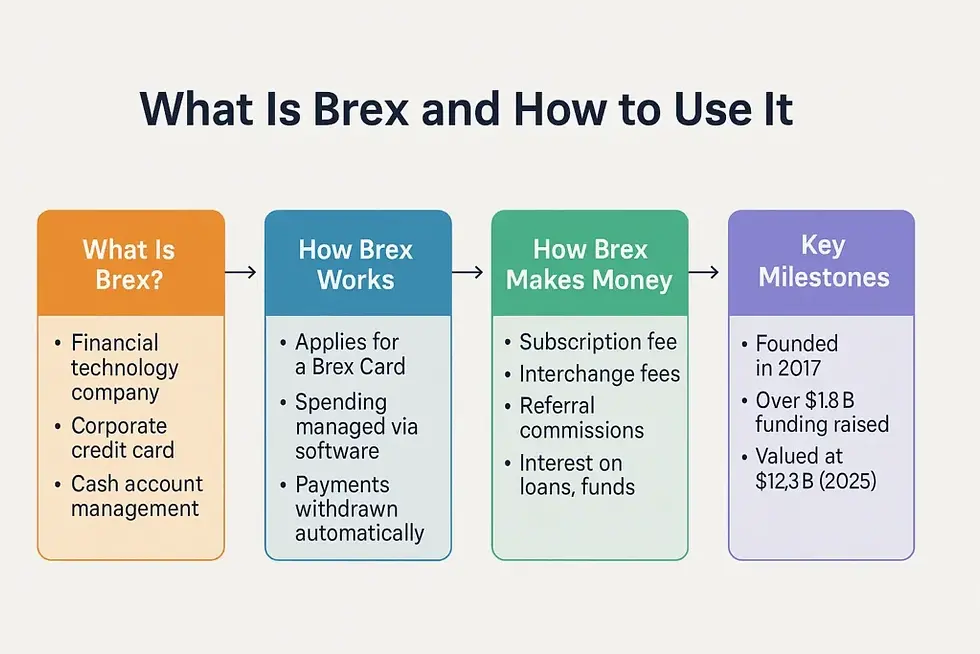

Brex began in 2017 with a focused pitch to venture‑backed startups that struggled to secure traditional corporate cards. Over time it evolved into a broader operating platform for business spend, combining corporate cards, spend policies, automated expense management, travel booking, real‑time payments and embedded B2B payment flows. Finance teams gained a single system where they could issue cards, set granular controls and see every transaction in context. That model attracted tens of thousands of businesses, a significant share of U.S. startups, more than 300 public companies and an expanding roster of large enterprises.

Capital One’s leadership has been clear about why Brex is strategically important. Richard Fairbank has described business payments as riddled with manual, error‑prone processes: invoices scattered across systems, approvals handled in email, card spend detached from accounting and reconciliation work that consumes finance teams’ time. In his public remarks he has credited Brex with building an integrated stack that connects corporate cards, spend management software and banking in a way that traditional bank offerings and standalone software tools have struggled to match. In that framing, Brex represents a purpose‑built technology backbone that Capital One can now bring into its broader ecosystem instead of recreating it from scratch over many years.

Brex’s CEO, Pedro Franceschi, has cast the acquisition as a way to compress time on the company’s roadmap. He has pointed to Capital One’s scale—hundreds of billions in annual card volume, a large asset base, a powerful U.S. brand and multi‑billion‑dollar marketing and R&D budgets—as the resources that can accelerate Brex’s mission by more than a decade. His stated ambition for the combination is bold: to build the most important financial platform for businesses in the United States. That ambition now sits on top of the Discover network, Capital One’s existing small‑business and consumer card franchises, and Brex’s software‑driven spending layer.

For merchants and B2B sellers, especially those outside the U.S. looking in, this is a structural shift in who will control the rails, rules and interfaces that govern corporate spend. A bank that already owns a major U.S. card network is bringing a modern corporate spend platform in‑house as a strategic core. Finance teams using that stack will operate inside integrated systems that jointly control card issuance, approvals, budgets and payment methods. As those systems spread, they shape how buyers decide to pay suppliers, which instruments they favor and how tightly they enforce rules around who can spend what, in which markets and on which rails.

How to Position Yourself in a Capital One–Brex World

The closing and integration of this transaction will take time, but merchants can start preparing now. U.S. corporate spend is moving toward a smaller number of powerful platforms that combine issuing, network access and software in one place.

A useful starting point is to map how much of your revenue depends on U.S. business customers paying with corporate and virtual cards, and how often those payments already pass through modern spend tools. From there, it becomes important to review your ability to accept and reconcile large card‑based invoices, support recurring payments, and provide clean transaction data that drops smoothly into customers’ expense and ERP systems. Payment partners and acquirers who understand corporate cards, cross‑border flows and integration with expense platforms will be valuable allies as this landscape shifts.

Capital One’s acquisition of Brex is being reported as a notable bank deal and a major fintech exit. For merchants and B2B sellers, it represents something more fundamental: a consolidation of network, issuing and software that will influence how U.S. businesses organize their spend and how money flows through the system. Companies that treat this as a strategic signal and adapt their payment readiness, data capabilities and operational flexibility will be better positioned as the new corporate spend stack in the U.S. takes shape.

From Startup Card to AI‑Native Spend Platform

Brex’s trajectory started with serving underbanked startups and technology companies; its product has since matured into a full AI‑native spend management environment. The platform supports corporate and virtual cards, policy‑driven approvals, automated categorization, real‑time controls and connections into accounting and ERP systems. In recent years, Brex has broadened its footprint to include travel and expense, embedded B2B payments and real‑time payment options layered on top of its card offering.

This evolution has carried Brex beyond the early‑stage segment into a client base that spans high‑growth technology firms, mid‑market companies and large enterprises with complex, distributed spend. The company has also invested in a vertically integrated technology stack, building infrastructure from the lower layers of payments and data all the way up to user‑facing workflows. That architecture is designed to support AI agents and automation, allowing the platform to handle complex workflows with less manual intervention from finance teams.

Brex has also signaled global ambitions. The company secured a license to operate across the European Union, enabling it to issue cards and deliver its spend management products directly in 30 EU countries. It has pursued partnerships to power embedded B2B payments in large software ecosystems and announced plans to support stablecoin payments linked to its global corporate card. By the time Capital One stepped in, Brex was positioned not only as a U.S. corporate card provider but as an emerging operating layer for cross‑border business spend.

Why Capital One Is Pushing Deeper Into Business Payments

Capital One is pairing this acquisition with a broader thesis about the future of business payments. In recent commentary, Fairbank has described a business payments market on the order of $2 trillion in annual purchase volume, expanding as companies move away from checks and cash toward digital instruments and structured workflows. Historically, Capital One has been a major player in small‑business cards, particularly in segments where the business owner is personally liable for repayment. Its presence in large corporate liability programs and end‑to‑end spend management has been more limited.

Brex fills that strategic gap. By bringing Brex under its umbrella, Capital One gains a platform that already serves corporate‑liability programs, mid‑market and enterprise accounts, and heavily software‑mediated workflows. The acquisition also complements the Discover transaction. Discover gives Capital One control of a major U.S. card network; Brex supplies a modern front‑end and control layer for business spend on top of that network and Capital One’s existing issuing capabilities. The combination positions Capital One to function more like a vertically integrated operating system for business payments, similar in spirit to some aspects of American Express, but anchored in a technology‑first approach and a broader customer base.

There is also a technology rationale that goes beyond card volume and client lists. Fairbank has frequently emphasized the importance of rebuilding bank technology stacks from the ground up. Brex brings a production‑tested, AI‑forward stack that can support more than just corporate cards. Over time, the same infrastructure can inform and accelerate other parts of Capital One’s business side, from small‑business banking to cash management and integrated payables.

What This Means for Merchants and B2B Sellers

For merchants and platforms that sell to U.S. businesses, the impact of this deal will be felt in the way customers manage their spending and payments over the next several years. As a Capital One–Brex stack rolls out, more finance teams will manage budgets, approvals and payment preferences from a single, rules‑driven platform. That environment favors vendors who can align with structured, software‑enforced purchasing behavior.

When a corporate buyer runs spend through a system like Brex, the platform can define which cards or virtual cards are used with specific suppliers, how limits are set for individual employees or teams, and how cross‑border spend is routed. The system can also require more detailed transaction data to support automated reconciliation and real‑time reporting. Vendors that are easy to add as approved suppliers, accept the corporate and virtual card products buyers prefer, and provide the right data and invoice structure will fit neatly into those workflows. Vendors that rely on inflexible payment terms, limited methods and manual reconciliation will encounter more friction as buyers standardize around integrated tools.

The acquisition also reinforces a trend toward platform‑centric B2B payments. Brex has already been moving beyond cards into embedded payments inside ERP and procurement systems. Coupled with Capital One’s balance sheet and marketing reach, that approach can push more B2B transactions onto rails that are tightly integrated with spend management. Large buyers may increase their use of virtual cards tied to specific invoices or subscriptions, and may favor suppliers that support these instruments efficiently, including in cross‑border contexts.

For international companies targeting U.S. corporates, this means understanding not only which card brands and networks U.S. customers use, but also which spend platforms sit between the buyer’s budget and your receivables. Alignment with those platforms will influence how often you appear as a low‑friction vendor in their eyes.

Comments